THE FED MEETING

This week is full of potentially market-moving news. The Fed’s two-day meeting begins Tuesday, with their Monetary Policy Statement and press conference coming on Wednesday. We know the Fed is hiking by 0.25%. The question is, will they hike again after that this year? The statement and press conference will have an impact on the bond market, and mortgage rates. The PCE inflation report is due Friday. The Fed favors this report. If inflation continues to trend downward, the likelihood of another hike will decrease. The market is expecting the Fed to pause. If the Fed gives any indication they’ll hike again, you can expect an unfavorable reaction.

The current Fed Funds rate is 5.13%. This week’s rate hike will take us to 5.25-5.5%. As a reminder, what goes up, must come down. I linked an article below to help you understand this trend as it relates to the Fed. In my opinion, we have yet to see the upward shift in unemployment needed to predict accurately when rate cuts will begin. The Fed was holding interest rates at 0% not too long ago in response to the Covid crisis. When you think “rate cuts” you have to remember it’s a strategy used to stimulate the economy. We are still in the middle of slowing the economy down to achieve price stabilization. The Fed will not make hasty decisions. The best case scenario creates an environment where prices and mortgage rates stabilize, while the job market cools down.

I’ll be back Wednesday with a detailed update, stay tuned in!

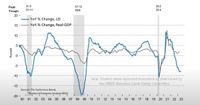

We discussed The Conference Board Leading Economic Index on the webinar. The composite indexes are the key elements in an early warning system to signal peaks and troughs in the global business cycle. The LEI anticipates (or "leads") turning points in the business cycle. For the first time since 2007, we’re seeing 15 consecutive months of negative growth. The chart below indicates a recession is on the way.

The NBER's Business Cycle Dating Committee defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in production, employment, real income, and other indicators.

RECESSION Q3 2023

A “soft landing” is a moderate economic downturn following a period of growth. The Federal Reserve and other central banks aim for a soft landing when they raise interest rates to curb inflation. That’s the goal.

A recession can have significant impacts on the housing market, affecting various aspects of the industry, including home prices, sales activity, housing demand, and overall market stability. Here are some of the key ways in which a recession can impact the housing market:

1. Decline in Home Prices: During a recession, there is often a decrease in housing demand as potential buyers become more cautious about making significant financial commitments. With fewer buyers in the market, sellers may need to reduce their asking prices to attract buyers, leading to a decline in home prices.

2. Reduced Home Sales: As consumer confidence wanes during a recession, the number of home sales typically decreases. People may delay their homebuying decisions due to uncertainty about their job security and economic conditions. This decrease in sales activity can lead to a surplus of homes on the market.

3. Increased Foreclosures: Economic downturns can result in higher unemployment rates, making it challenging for some homeowners to keep up with mortgage payments. This situation can lead to an increase in foreclosures and distressed properties hitting the market, further contributing to declining home prices.

4. Tightened Lending Standards: During a recession, lenders may become more cautious and tighten their lending standards. It can be harder for potential buyers to qualify for mortgages, reducing the pool of eligible buyers and further dampening demand.

5. Slower New Construction: Homebuilders may scale back on new construction projects during a recession due to decreased demand and difficulty in obtaining financing. This reduced supply of new homes can impact overall housing inventory levels.

6. Impact on Home Equity: Homeowners' equity can be eroded during a recession if home prices drop significantly. Negative equity situations, where homeowners owe more on their mortgages than their homes are worth, can lead to higher default rates and foreclosures.

7. Shift in Demand for Rental Properties: Some potential homebuyers may opt to rent instead of buying during a recession, leading to increased demand for rental properties. This shift in demand can result in higher rental prices and increased competition in the rental market.

8. Regional Variation: The impact of a recession on the housing market can vary by region, depending on the local economy and industry composition. Some areas may experience more significant declines in home prices and sales activity, while others may remain relatively stable.

Which of these outcomes are likely in a low inventory environment?

The compression in supply is what’s keeping the housing market safe. Until mortgage rates improve, it’s not likely that homeowners with low rates will be inclined to sell, unless they have to. The US population is 19% higher than it was in Jan 2000 while the inventory of existing homes for sale is down 37%. The median sales price is now less than 1% below their peak last year. Demand decreases in the Fall and Winter, but competition will remain stiff if we don’t add to the supply.

Many expected huge price declines this year. The number of home sales are down for 22 consecutive months. The longest streak since 07-09. New home sales are experiencing record highs. Home prices remain stable.